Credit Card Companies: We Charge You Late Fees Because We Care About You

Credit Card Companies: We Charge You Late Fees Because We Care About You

Biden Administration Seeks To Lower Late Fees on CCs to $8 - Banks Have Lazy Excuse to Defend the Practice

First off. Thanks for the love and support about “Stale Coffee Breath”. So many people who I was sure would turn on me for writing it actually didn’t, and many of you are sharing it. Means a lot to have my research validated by you all. Please tell your friends to sign up, and help me make a living on this writing gig, along with my other stuff!

Share it with friends. I made a domain for it. StaleCoffeeBreath.com. Have them subscribe too!

There’s a reason I call myself a “Consumer Advocate” and not a “Financial Expert”. It’s because I am no financial expert. I actually fucked up my credit with student loans 13 years ago, and have maxed out a couple credit cards just before BofA fired me. I have big bills which I don’t fear, but I also hate that I did that to myself like a lot of Americans. I intend on paying those off through hard work as The Notorious Banker and through the support of people who like my work.

If I was a whiz in finances, I wouldn’t be in that boat. Guess what? That debt load would likely DQ me from any bank jobs. I learned my lesson, I pay my bills like an adult, but according to a credit score and a bunch of numbers, I’m not to be fucking trusted.

It’s ok, I’d rather steal catalytic converters than work for a bank again.

But that being said, I am an advocate because I can see how the excessive fees and bad credit reports impact Americans as a whole, because I was sitting in front of these people for 13 years. Banks beat the shit out of you by nickel and diming you, and then telling you that you aren’t worthy of their help to buy a car or a home.

Per a WSJ article today, and talk by the Biden Administration over “illegal fees” in all walks of life, the Administration is proposing a rule that would cap the amount of a credit card late fee to $8 per month. The fees range from $19 on up. Discover, who is routinely praised for their customer service charges $41 a month, and you can’t even use that card everywhere. I know Chase from personal experience charges $28 on my Amazon card. (More on that later)

It’s not a lot of money, but it is a kick in the groin to someone who may have had a reason they couldn’t get to it. What if you have sick kids in the house? What if a family member died and you spaced out? What if the bank’s system messed up? Why should you be punished for life’s little hurdles.

Trust me when I say late fees are NOT a big source of revenue. But think of it this way, if you come up to me and ask to have one of my 70 soft drinks in my garage, I would not want to give them to you. Those are MY vanilla Dr. Peppers.

Banks are like “THIS IS OUR REVENUE! We don’t want to give it up.”

When I post on Twitter or Tiktok, there’s always some holier than thou person that preaches “personal responsibility” while defending big banks being assholes about recovering $35 from a person with no money.

These are the same people who claim to support small businesses while buying a 30 pack of Bud Light at Walmart with a Bank of America card in their Nike Wallet.

Dude, I may have fucked up my credit score in my 20s, but now that I am a freelancer, I have to be uber responsible to survive. I would not willingly ruin my credit any more, much less to avoid a $35 fee.

So, a few months ago, I was charged a $28 late fee by Chase. I didn’t know I got a late fee on that card until I started getting a bunch of weird calls on my phone. Usually I get those from being on mailing lists from here to NYC, but these were specific numbers. I traced it back to Chase customer service. Instinctively, I went to my online banking, to see what was a $28 late fee.

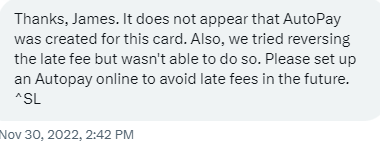

Here’s the thing: I had it on Autopay since 2011. I also had a good amount of money to cover $35 in my account. When I looked at that particular card (I have 3 of them), I noticed Auto Pay was turned off. After being furious, I reached out to Chase on social media for help. It was outrageous that I even had to do that. I explained what happened, and what occurred in a bank-y way to help them along.

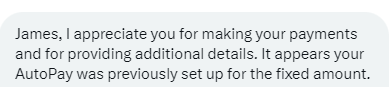

Then they told me that they DID locate the error Chase made in inadvertanly toggling off my auto pay and they apologized to me for it!

….But they didn’t waive the fee. I was still out $28 and a mark on my credit for 7 years because of it.

LOL. “We see that there was a previous AutoPay set up for this card. Then next message “It doesn’t appear Autopay was created after all”

Then the best part. “Can’t waive the late fee…perhaps you should have had autopay” LOLOLOLOLOLOLOL.

You fucking kidding me?

What? Why?

They wouldn’t give me a clear answer as to why they wouldn’t waive the fee. I know from my Bank of America days that a lot of the times an alogrithm chooses to favor “preferred” customers on fee waivers, and as fucking highly as I think of myself, I am not preferred. I am gloriously average.

I was furious and now I troll them any time a Chase story comes up. I am petty like that, and frankly, I don’t care. People need to know what happens to some folks with credit cards.

Now, $28 isn’t going to break me, it’s the fact that I was responsible enough to do a payment plan, and they turned it off and blamed me for it. 11 years, it never screwed up until it did. The “convenience” they sold me on was gone and then they are like “Why didn’t you check your account and pay it yourself?”

STUPID.

Back to the Biden plan. No I am not going to hear political shit from either side about this. This isn’t that kind of blog. Go wallow in the muck somewhere else if you want to make it political.

The thought is these fees are illegal, because it punishes people who may have a valid reason that they didn’t make the payment, and all things being equal, $41 late fee is not as bad as the 7 years on your credit report. Two marks on your credit report and an average credit score means good freakin’ luck getting approved by underwriters for a home at a big bank, even if it was a $35 fee.

Jodie Kelley, who is the CEO of the Electronic Transactions Association, who basically is a lobbying arm of big banks had the DUMBEST quote in the WSJ article I shared above.

(P.S. I am sure she is a nice lady when she is not associating herself with companies that pillage poor people on a daily basis)

“By almost eliminating the fee, it could increase the number of late payments, which harms the credit worthiness of the consumer,”

LOLOLOLOL

I want to do a chef’s kiss for that take that she had. It’s stunningly full of poop.

So, the argument from her is “More people will be late on their credit card payments because it’s only an $8 fee and we want to protect their ‘credit worthiness’ by keeping the fee high”

She’s basically saying the $40 fee is a knife at the throat of the consumer that keeps them honest and keeps them paying their bills like a good little consumer. Why does she care about their credit worthiness?

Because the banks she represents don’t want you to be encouraged to fuck up and miss your payment so you can be of use to them in the future. How? Well, if you have a good credit score, you will go to their banks to buy a home, giving them more money, you will go to them to buy a car, giving them more money, and you will get a second, third, or fourth credit card, giving them more money in revenue.

You are a concubine of the banking industry, and their threat if you leave is “We will charge you $40 AND FUCK UP YOUR CREDIT if you don’t pay us, so we can finance more things for you”

It’s for their own self-interest. It’s not to protect you.

I had the weirdest analogy, and I am going to share it. I have been around people who committed or been a victim of intimate partner violence in my time. Friends, family and coworkers. I have seen it all my whole life.

In the machismo-based Chicano culture I come from, there’s a type of abuser that is common. It’s called a food control abuser. Basically the perpetrator tells the victim that the victim is too fat, so they need to eat less to lose weight. They control the food they eat and punish them if they don’t comply.

Conversely, there is a type of abuser who thinks the other way. My significant other looks too good. I want her to put on weight so they don’t look at hot so they will be mine forever and no one will want them. They also control food intake on their victim.

What a fucked up analogy right? I hate using it, but it’s basically the same thing. PAY YOUR BILL OR WE WILL FUCK UP YOUR CREDIT. They only want to keep you healthy to use you to sell you more products to put you more in debt.

How is that not abusive?

If Biden’s administration has their way and lowers the late fee, guess what? an $8 fee will fuck up your credit anyway, because it’s late and impacts your credit score, a thing that was made up in 1989 by FICO to basically rate people like it was a dating site.

FICO is basically the old Hot or Not website where people gave you a score on hotness. Facebook was basically that in its infancy.

Note, 20 years ago in 2003, I was a 7.9 on Hot or Not, and I swear to you, it made my year and motivated me to get in shape to be hotter for my budding dating life.

I was in the business of trying to offer home loans at Bank of America, and I would see a person with a 670 credit score, minimal debt, maybe a hiccup here and there over 20 years NEVER get approved for a home/auto loan.

They can’t raise it up because they don’t have enough credit lines. They can’t get enough credit lines because they missed a payment 5 years ago, but they never missed a payment otherwise. It’s a game they play to string along those they don’t want to deal with and Jodie Kelley is basically defending their fees as saying “We do this to help you”.

Give me a break.

It’s like giving a spanking while telling them you do that because they love you.

I am a different man at 39 than I was at 26, when I defaulted on my student loans. All I cared about was boobs, boxing, and Vegas back then.

(Note, I was losing hair at this point. Don’t know why I didn’t shave it all off then, especially next to porn star Jesse Jane)

I am a different man than I was at 18 when I got my first credit card. All I cared about was boobs, pro wrestling, and Madden NFL 2002 back then.

My create-a-team was called the Socorro Shotas, a name I use to this very day for my Fantasy Football. Chotas (Shotas as I misspelled it) is a Mexican slang for “Policeman”… though if you Google “Shotas” you will get a NSFW meaning. My bad.

What I mean was I am more mature now than I ever was then, yet big banks gave me $15,000 in credit card lines that I used up. But you will have the audacity to punish me and my credit worthiness because of a system glitch, a $28 fee you won’t refund disregarding 21 years of having credit, not to mention getting paid by a bank to talk about the benefits of credit for 13 of those years? Gimme a break.

I propose a compromise. You might be surprised by it. I really don’t care about the $8 cap on the late fee. $8 can’t even buy you a Whopper Whopper Whopper Whopper, Junior Double Triple Whopper value meal at Burger King. (YOU RULE!)

Keep it at $40. But do me one favor. Don’t call the late fee a strike on someone’s credit report until after 90 days. Shit can happen in a 28 day credit card cycle that can throw you off track for weeks, meaning you neglect bills. People get sick. People die. Depression. Family obligations. Etc.

If you truly want to help low and middle class people experience home ownership, and if you want to counsel people of color into having a better financial outlook to do things their elders never did, then eliminate that punishment for forgetting to do something one month that if you did it today would linger on your credit report until March 1, 2030… and even then, though banks would never admit it, they will still use it against you.

Biden and his administration has the right idea about these fees, but I think the execution is a little off. The late fee revenue that banks make is like the couple bucks of interest they throw at you for having $15,000 in savings account. It’s something, but it’s not everything. They don’t make or break their bank on it, so them defending it saying it is there to help people is stupid.

I want people to realize the importance of their credit, but don’t fucking listen to a hack who represents big banks in Washington telling you that the fees are there for your protection.

People who say stuff like that should work at a Burger King for a few months with some people in their 30s that can’t catch a break because of credit fuckups in their 20s. Get paid like them, worry about the next meal you eat and where it’s coming from and then sing…

Eat like a king who's on a budget,

Three tasty options, fries, drink and nuggets

All for $5 wait that cant be right

Just confirmed that thats the real price

AT BK…Have it your way! You Rule! (Except for big banks and lobbyists who carry their water)

-James