FARMing OUTrage: Support Small Businesses, Not Credit Card Surcharges That Small Businesses Claim Helps Support Them

FARMing OUTrage: Support Small Businesses, Not Credit Card Surcharges That Small Businesses Claim Helps Support Them

Local Southern NM Restaurant Angers Customer Base By Charging 3.5% Credit Card Fee - Why Dealing With Cash is No Help Either

There’s not a person on God’s green Earth that put forth the effort I did in telling a crazy story that WILL get noticed very soon in local media. I am letting it simmer if you will.

I do not want to neglect “Consumer Beast” because at the end of the day, talking about banking, business, and customer service are my bread and butter. I love discussing ethical decisions and customer experience with people who didn’t realize no one talks about it quite like I do. So thank you, and please, if you found me through AGGregator, please subscribe here as well.

NOTE: To my new Las Cruces-Based Subscribers. This column is based on my expertise as a financial/banking/customer service expert. I only write these things to help, even if it means I will never go to their place of business. Sometimes tough love is needed, and they need it here.

So, I am not a big eating out kind of person. It first started to be that way when I lost my banking job in 2018. I was someone who didn’t want to see old coworkers or old customers, although I was almost universally loved by everyone. 2019, Money started running low, so I created The Notorious Banker and made a living helping people with bank and customer service issues using a brand of “training” that is unlike any other person doing what I do. I used my money to pay bills and that was it. Very rare I would eat out

2020…”Unprecedented Times” happened. Don’t you miss people saying that phrase? Businesses were forced to close. Restaurants could not have in-person guests, and when it started to loosen, especially in New Mexico, which had some of the tightest restrictions, it was 25-50% at best until literally the beginning of 2022. Some businesses didn’t make it. It was sad. Some businesses got PPP and EIDL loans, and actually made money. Me? I made money during COVID. Why? Because I had the smarts to understand what was available to me. But me and my wife limited our eating out to once a week, usually Friday night, calling it “Friday night bites.” Of course, it would be a rule relaxed by vacations and travel.

Not going to fault anyone in doing what it takes to survive during that time. But with 2022, 2023, and now 2024 in our not-too-distant past, present and future, I have seen a retelling of how hard it is for “small businesses” out there in today’s market.

Sh*t like $10 a dozen eggs? Yes, that sucked. It was not fun for me or my niece, Aaliyah who liked “Beans and Eggs” for breakfast every morning. I am sure my mom is in hock to loan companies still off of that. The cost of gas goes up and down. Ugh. Though, I normally never complain about gas.

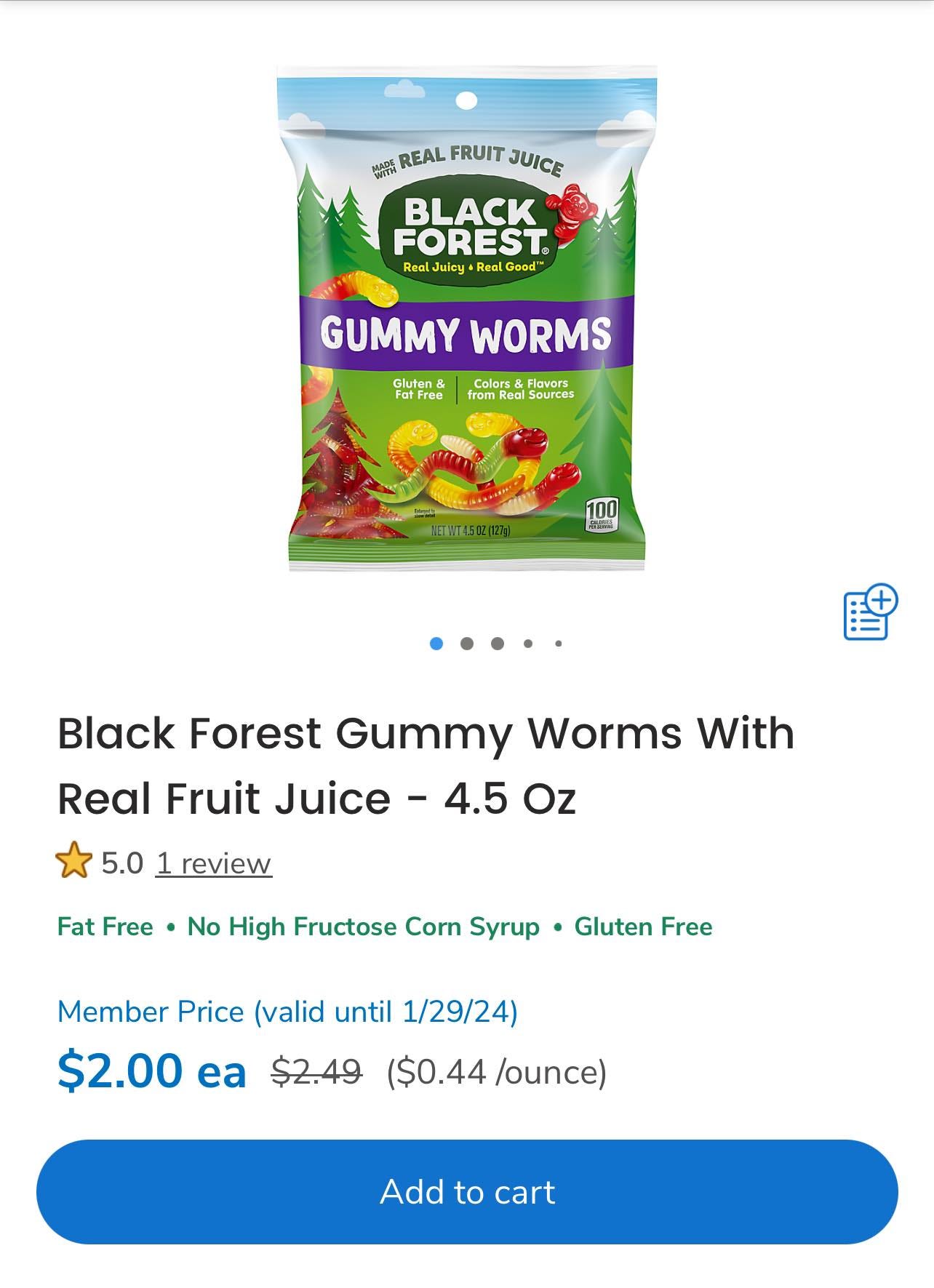

What about the cost of groceries. Now, I can get with that. Stuff has gone up in price. My beloved Black Forest Gummy Worms used to cost $1.19 at Albertson’s as of 2017. Then $1.29 in 2018. $1.79 in 2020. $2.19 in 2022, and my dear lord in heaven, $2.49 currently (though they are on “sale” for $2.00 now). I hate it so much. 2x the price for slightly less gummy worms in a bag.

My beloved Vegas trips were always defined by a craving for this snack. A trip to one of the 102 pharmacies on the strip would find me paying a price gouging price 5 years ago of… $2.29 in Vegas. The normal price is now the f-ing price gouging 2018 Vegas price. I got so mad. People should be mad at things like that, and no matter if you support big business, you should protest the Albertson’s-Kroger merger, because it is going to be like Hawai’i prices for food soon, and that won’t be fun.

Small businesses, who have to deal with cost increases from their vendors, or some who go to the store for supplies every day, have it hard. It’s no fun to have to deal with the cost of that going up, paying employees, and paying bills. But it’s part of doing business. You have expenses to do anything? You want to save gas money by getting a tesla? It still costs to charge up your car, though. You are just moving expense from one box to another box.

Now, with Consumer Beast, I have made it my M.O. to be confrontational usually, but I am going to try to be more like Robert Irvine. Firm, an asshole, but full of wisdom and knowledge from a life that has taught me a lot.

I want to do that with FARMesilla, a local eatery and gift shop in Mesilla, NM, which is in Dona Ana County, NM. It opened in 2018 and in the course of 5 years has a pretty good fanbase of people who love the idea of something like FARMesilla, because it is unlike anything in our area.

One of the cooler things about being married to my wife is she likes to try new things, and eat fancy foods, or something our parents and grandparents wouldn’t eat or touch with a ten foot pole. We like trying things out of our comfort zone.

These are two things I immediately go crazy for… because how I grew up, we would never eat blue corn, blackberries, or even whipped butter. We wouldn’t eat anything “espresso” flavored or know WTF a ganache was. Ganache looks like it is something you would use to talk shit to someone else with in spanish.

You pinche ganache (pronounced gan-atch-ay) son of a bitch!

But yeah, these are things my wife and I love and in a world where we ate out more, we would try everything on their menu and when we fell in love with something, we would always go back for that go-to bite we love. If I had money to eat out every day, I would, and would support non-chain restaurants, because I like supporting small business and I like creativity of others in their craft.

Never heard a bad thing about FARMesilla, aside from the usual “it’s expensive.” I don’t like comments like that, because I don’t know how much blue corn waffles SHOULD cost, so if they say they are $9, I am going to take them at their word, you know? I could buy Aunt Jemima (or whatever the new name is) for $3 and not get a “OMG this is insane” bite!

They have a 4.9 rating on Google, and again, universally loved by who is around there, and Mesilla is full of rich people who want eclectic meals, poser rich people who want to pretend they are full on rich people, and let’s face it, the newer generation opened to farm to table mentality, obscure ingredients, and the desire to be different.

If you are providing a novel meal, charge what you want, because I BET no one will try to match your uniqueness. Look at their menu. There’s no “Just a plain ol’ f-ing burger” or a “Straight down the middle hot dog” or a “Blah Blah side salad.”

Everything is something, and only someone meticulous with their desire to be different, and willingness to put in the effort on meals like that tells me that person is one in a million, and I commend the proprietors of that place for that. You are unique and amazing.

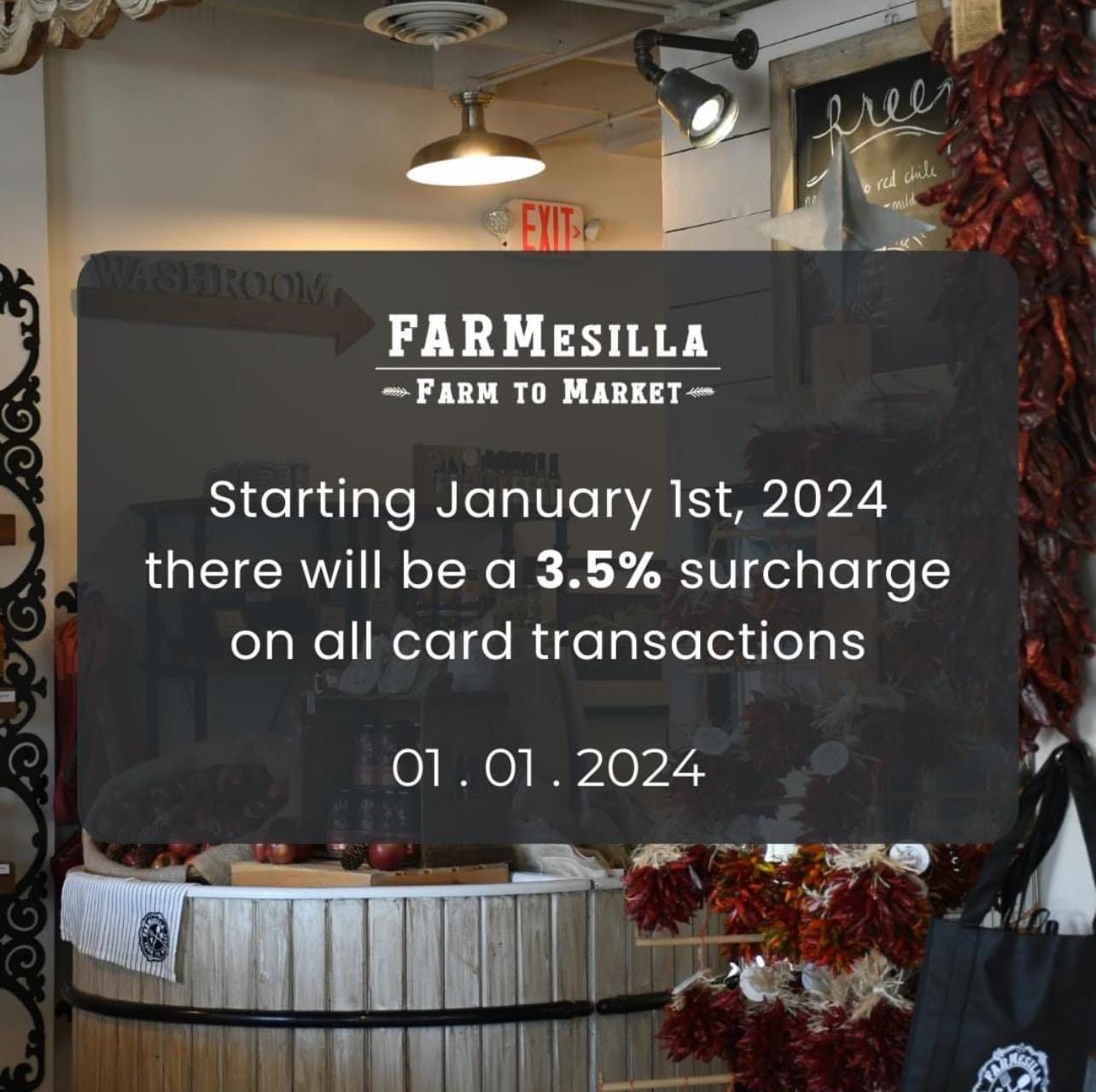

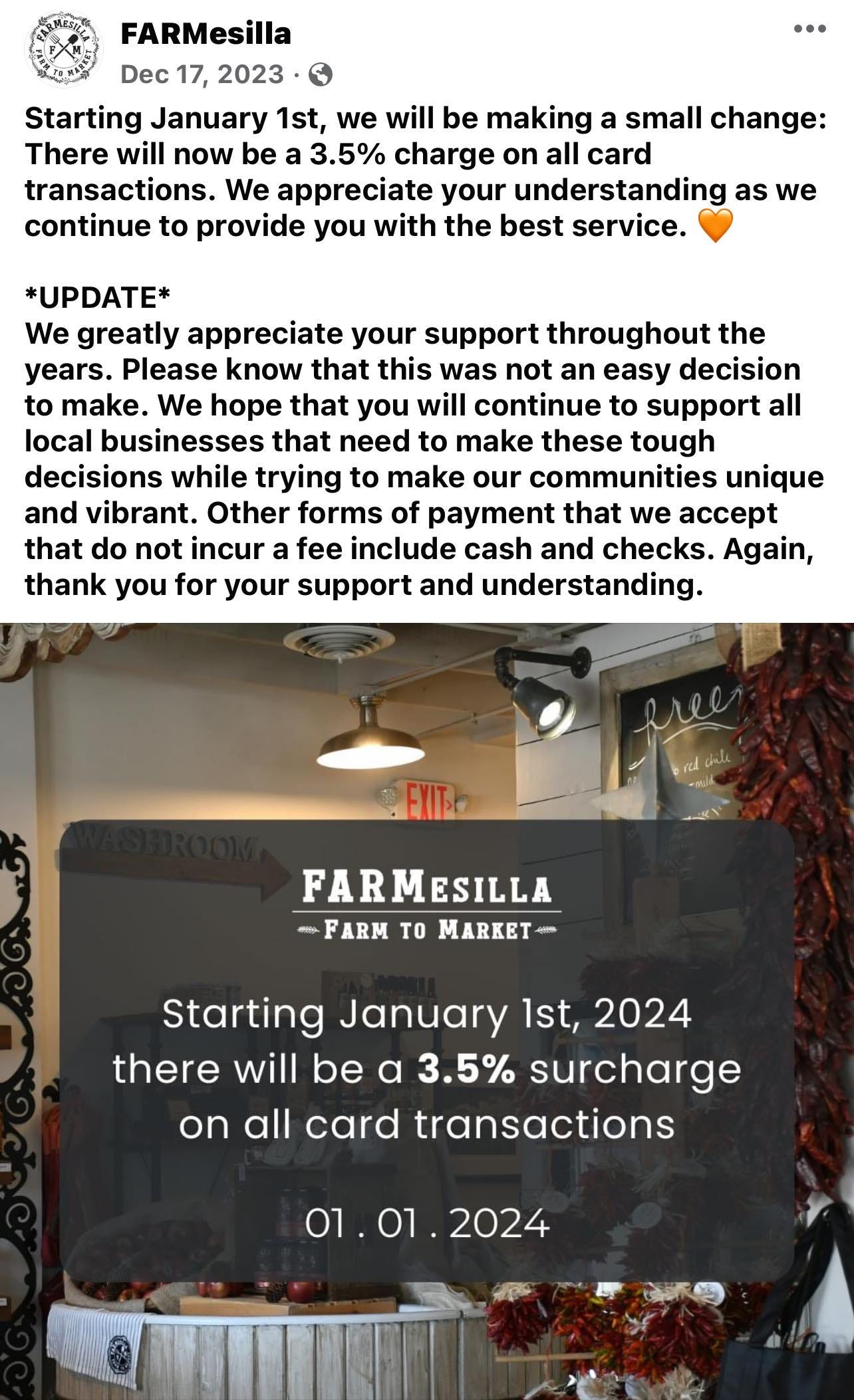

This…this is not unique and amazing:

No. No. No. No. No.

3.5%?!?!?!?!?!

No. No. No. No. No.

Watch this from :25 to :35 to get what I was going for..

3.5% ???

Why? Why now? What changed?

Now, as a former banker I am going to school the general public on why convenience charges for using your cards are a total scam and a cash grab for someone looking to buoy declining revenue, while PROVING to you that making people use cash or checks is actually just as bad for the business for all the same reasons they claim.

This was FARMesilla on Facebook.

This isn’t a tough decision. This is an ignorant money grab. Here’s why.

So, as mentioned before, I am a dumb-ass who worked as a teller, banker, and manager at Bank of America for THIRTEEN OF MY FORTY YEARS AND MY GODDDDDDDDD, THEY WERE AGONIZING. I loved helping people. I hated hurting people as a result of my bank sucking so bad, and I learned a lot about the day to day operations of businesses, restaurants, and more importantly, all the elements of how they bank and the types of services they need.

Businesses were my bread and butter. One business trusting you with opening accounts and using you for merchant services (accepting credit cards) can be up to 5% of your QUARTERLY sales goal on 1 person with 3 months in a quarter, you are well on your way to success.

Offer people checking accounts for business, savings accounts, business credit cards, and so much more, and I can literally smell my bonus like those waffles.

But I will tell you merchant services are NOT fun. I wasn’t the one selling the products to these people. My job was to refer them to another salesperson at the bank and those assholes (and yes, I need to use bad language here because they are fast-talking assholes who are looking to separate people from their money) are to sell them the newest credit card terminal, try to get them to buy blank cards to use as “gift cards” for their business, so the bank can make money on the fees for those, and so much more.

It’s not just a slide, tap, or insert anymore. It’s a whole thing now. They want you to be able to create mailing lists for your clients so they can come back for you and make you and the bank more money. It’s all really quite cool, if not intimidating. Normally this type of deal requires a background/credit check, a site inspection, though BofA used to have me fake those for the company, and get these crazy contracts signed which usually involves a lease of a bunch of bullshit equipment you don’t need mostly. Like I said they are good.

Those contracts are more meticulous than home loan closing docs, I swear. If you own a business and you dealt with BofA, WF, ADT, or someone like that (not square…they make it too easy tbh) then you know what i mean.

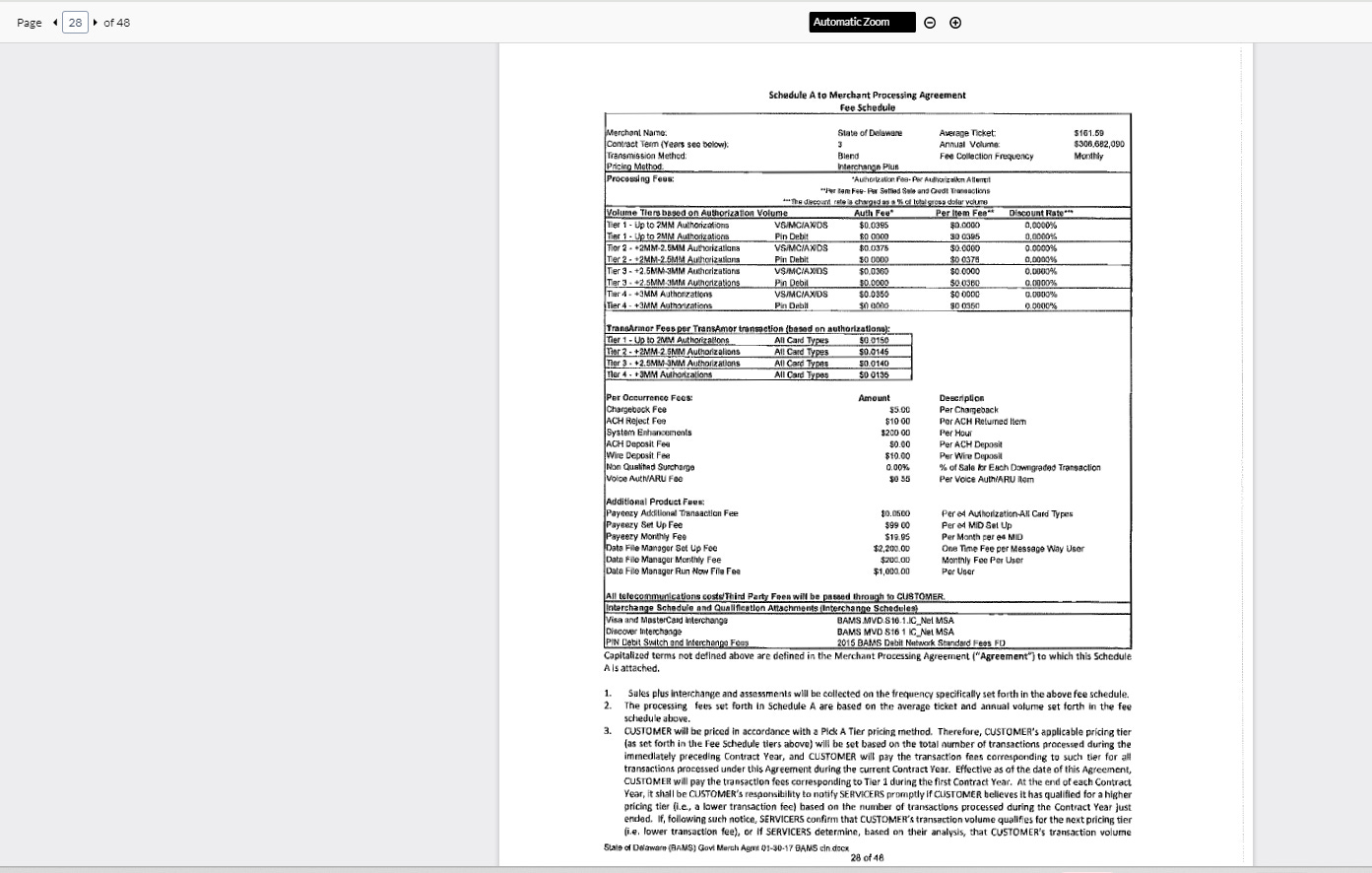

This is 1 page of 48 from the state of Delaware’s merchant agreement with BofA. It has different fees for different things. A fee for visa debit, mc debit, AmEx Credit card, Discover Card, International Visa CC, International Visa debit, Visa card if you have a unibrow, Mastercard if you haven’t been sexually active for 3 years. I kid about the last two, but long story short, there’s a fee for every card you can imagine, plus a schedule of fees if someone asks for a refund, claims fraud, etc. It’s a lot. It’s intimidating.

I don’t know what FARMesilla has for merchant services, but chances are it was a bank which gave them 48 pages like I mentioned.

So, I get it with the fee schedule, and I will get into it some more in a bit, but that agreement I referenced? It’s a contract, usually a 24-36 month term, and much like anything else in business SHOULD BE REVISITED at the end of every term. What happens with banks if you don’t put yourself through the wringer again and hunt for the best deal, you will get stuck with a rate that you may be uncomfy with because it went up or you were sleeping on locking in new terms. That’s on you.

Those contracts are almost always a fixed rate for the term of the contract. Very rarely are they variable rate. Not saying they aren’t out there, but I have been associated with the banking industry 20 years, and CANNOT think of one bank off the top of my head who does that.

So, let’s say for the sake of argument that their 3 year contract with… I dunno Stripe ended in 2021, and they didn’t do their research and got stuck with a payment processor that was not favorable to you and you signed something that was worse than before. That’s on you. Not on your customer.

The fees you signed don’t go up or down. They stayed the same, so to charge your clients 3.5% more because you didn’t do your homework is just wrong.

People were pissed.

It takes a lot for me to agree with Jamie Bronstein. I have never met her, but she is filled with some of the worst hot takes ever, including bad mouthing the kids of a murder victim last year (I have the screenshots because she deleted them). Not to mention her NM State Athletics takes along with the takes of her wanting the AD gone.

I mean it’s not ILLEGAL. She’s wrong there. She is right about passing on a fee that was their problem to the customers. Plus, I can tell you as a merchant service expert, 3.5% can be the fee on some high end rewards cards. The normal fee range for a business that is a “Small business” (defined by BofA as a 1mm-10mm/year revenue business) is in the sub 2% rate still even with everything going on in the world.

Like I said, the higher-end cards like airline cards, cash back cards and rewards based cards will be more expensive, but the rates I am giving here are pretty standard on a 24-36 month contract.

This is a good rule of thumb breakdown on a $100 tab with a “normal” rate of 2.5%, which is higher than I bet they get charged. Yes, you have 1000 people spend $100 and you lost $2,000, but you generated $97,000 in revenue. Cost of doing business like the employee you pay to slide a clients card.

Yes, consumers should know when you get those cool air miles credit cards to earn flights to Corpus Christi, the merchant pays the bank more for that privilege, which is where I will feel a little bad for FARMesilla, because people want to game their credit cards for rewards. Still, that’s a “blame the banks” not punish your clients.

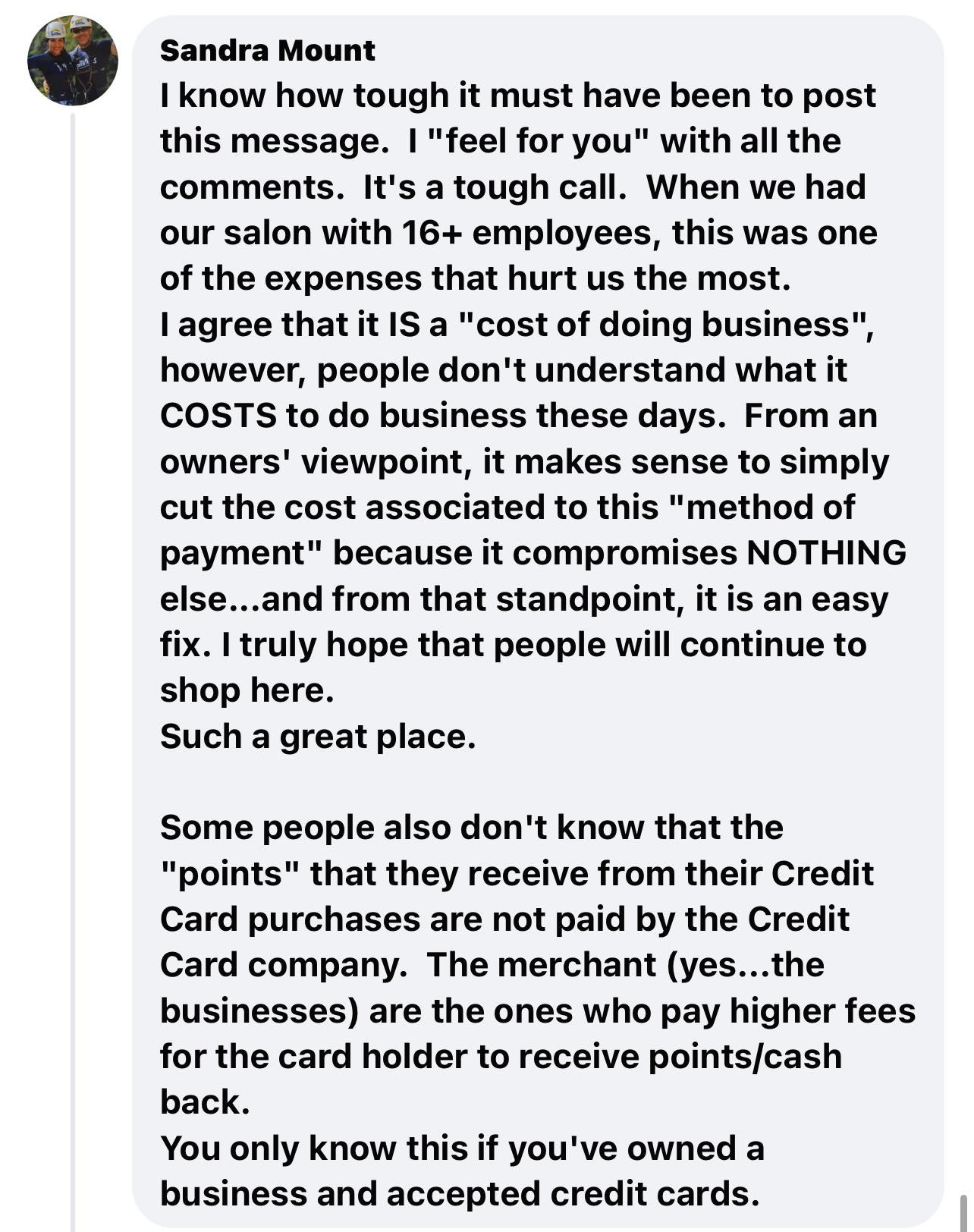

This person was empathetic to FARMesilla, but also acknowledged it’s the cost of doing business. She references “cutting the cost of accepting this method of payment” which is a roundabout way of saying “call your damn bank and try to fix this.”

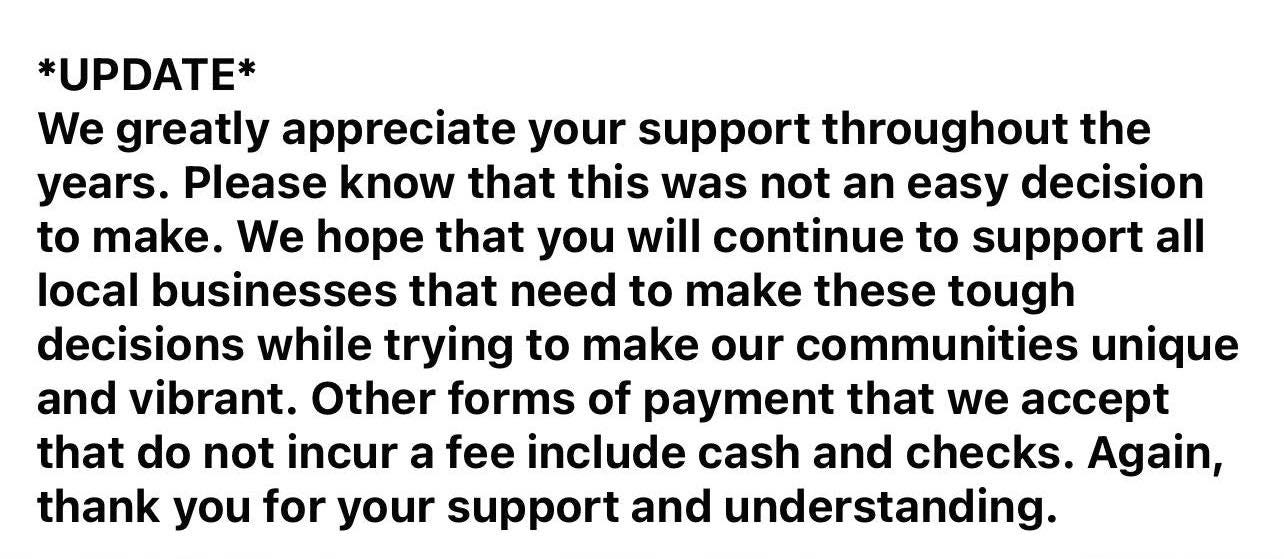

The “update” was as ignorant as the original post.

Ok.. So checks can bounce, and a fee is charged to the maker of the check, AND a fee is charged to the merchant, if you can believe that. Yes, banks suck and businesses lose their inventory and money because someone passed a bad check. I hate it too.

But again, accepting checks, and assuming that risk is more costly to your relationship from your bank as all banks deem restaurants “high-risk businesses” because of the ease of fraud that can happen there (stolen cc to pay for food, etc.)

Now the “We accept cash” thing. Ha.

I may be the only person who will ever point it out to people who read this or maybe even them.

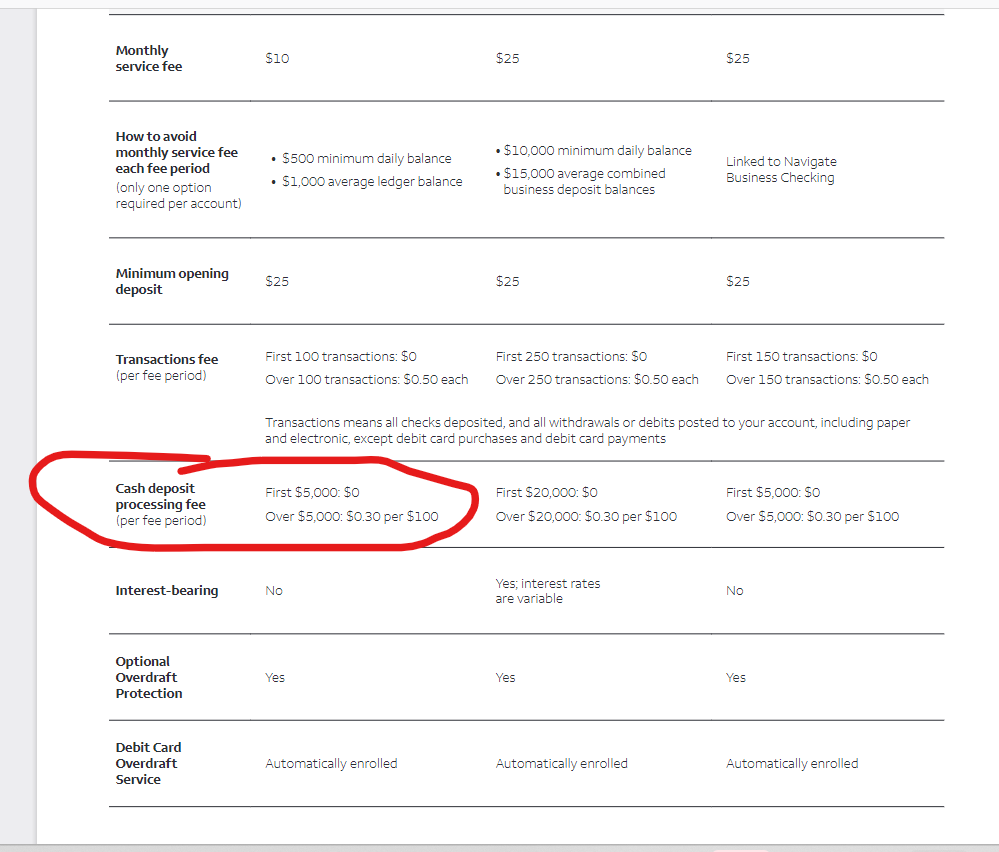

Depending on where you bank at, but usually most major banks, and especially smaller banks and CUs CHARGE YOU MONEY to deposit cash into your bank account. Businesses get charged a percentage

Now, it’s very rare that the cash deposit fee becomes an issue. It used to be for me when the movie theaters had summer movies and the theater chain that banked with us would get charged 1000s a month. So, I am not saying “they are going to lose as much money going to cash only,” I am merely saying that there’s a fee to deposit cash at almost any bank. Point me to a bank that doesn’t have that in their schedule of fees, and I will eat my hat.

Again, it’s not as much, but it is hardly the effective alternative, because it requires more bank visits, it can charge you for the excess cash + you have a deposit limit of x amount of transactions at most banks before you get charged for that.

Let’s not mention by pushing people to accept these options in lieu of using a cc just so they don’t bitch about the 3.5% fee, let me use an old pushback response I was taught.

CONSUMERS SPEND UP TO 83% MORE IF THEY USE A CARD OVER CASH

They aren’t always going to buy 2x as much, but you have effectively eliminated card person pissed about the fee from ever going crazy in your store, because they will be like, “Ok, $250…so I have to give them $8.75 more just because, even though my visa debit card interchange fee, which was utilized by entering a pin is 10 cents plus 1.5%. So I am giving them like $5 more for free even though they claim it is the banks fault and sUpPoRt sMaLl BuSiNeSs?”

Ok, that won’t be everyone, but that would be me, and I would choose not to buy a lot of stuff. I really would not, because I know that the fee is a result of their bad decision with their merchant provider or the bank and their way to rectify is actually does not save them money, so giving them cash would feed into their illusion of skirting said fees.

Nope. Can’t do it.

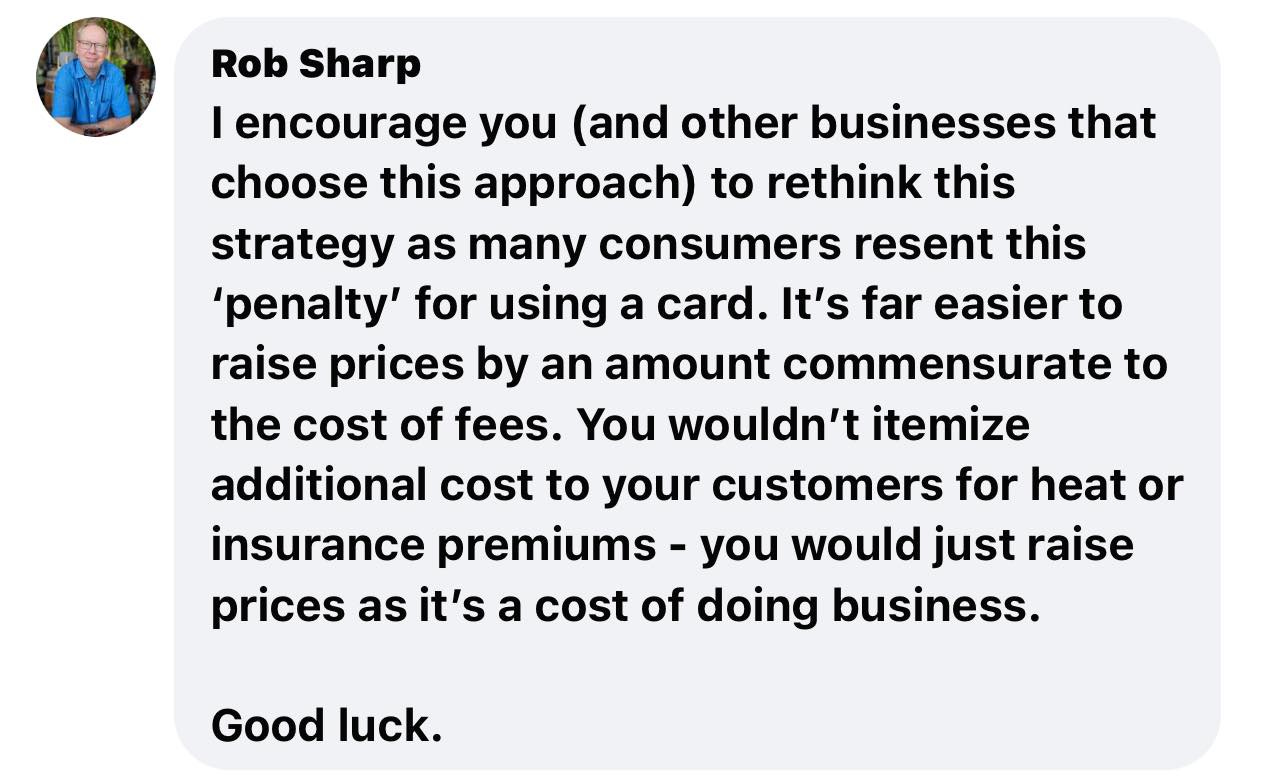

Rob Sharp was…the sharpest person about it.

Great point. Just raise your damn prices 3.5% even though that number is BS and people would have said, “Damn, Bidenflation!” Or if they are on the other side of things, “45 messed this economy up. These small businesses need to raise prices to survive. It’s tough out there!” (See, I was non-partisan in the outrage hahaha)

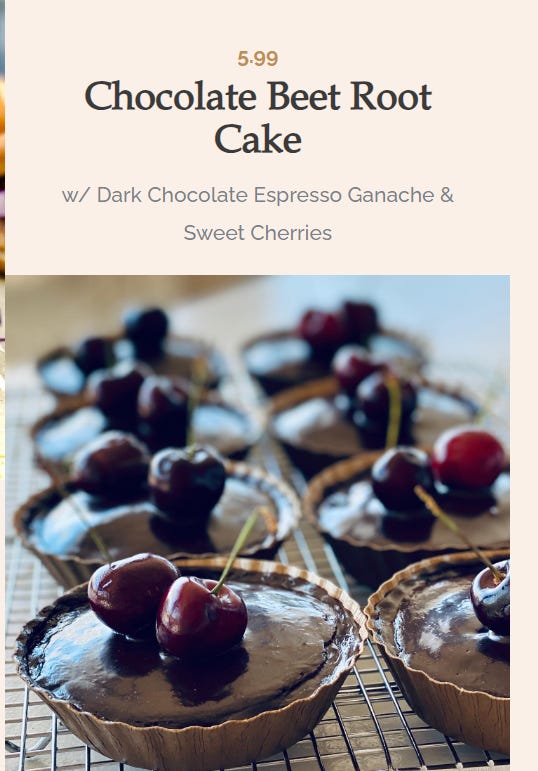

Let me show you the Blue Corn Waffles again:

Again, a lot of fancy stuff I can’t get most places and I GUESS $8.99 was an ok price for it. Kind of expensive, but what do I know, I am a consumer? (Smart consumer because of my training and expertise)

3.5% more for this - 31.5 cents meaning the waffles would be $9.30.. Just call it $9.25 and no one will know. I promise you. You got your 3% increase off your food to offset your alleged “cost of doing business” increase on the cc machine (not true). You win, customers kinda win, because you gave them one less thing to complain about and you could have gone on and be successful!

Rob Sharp’s comments echo my belief. There are ways you could have raised the prices 50 cents across the board and made more money on some things even based on that 3.5% number you quoted. Again, it’s not the money that is the issue for customers, it’s the fact that you are passing your bad banking experience onto them for doing what nearly every american and almost all euros and asians do in their countries, and that is use the card.

I am no ringer for big banks, I hate what they have become, and frankly, I am on your side when it comes to fees in this world, but there’s a right way and wrong way to come about this.

You offer really unique, niche items that I expect to be expensive, and likely got more expensive after 2020. I get that. It’s fine.

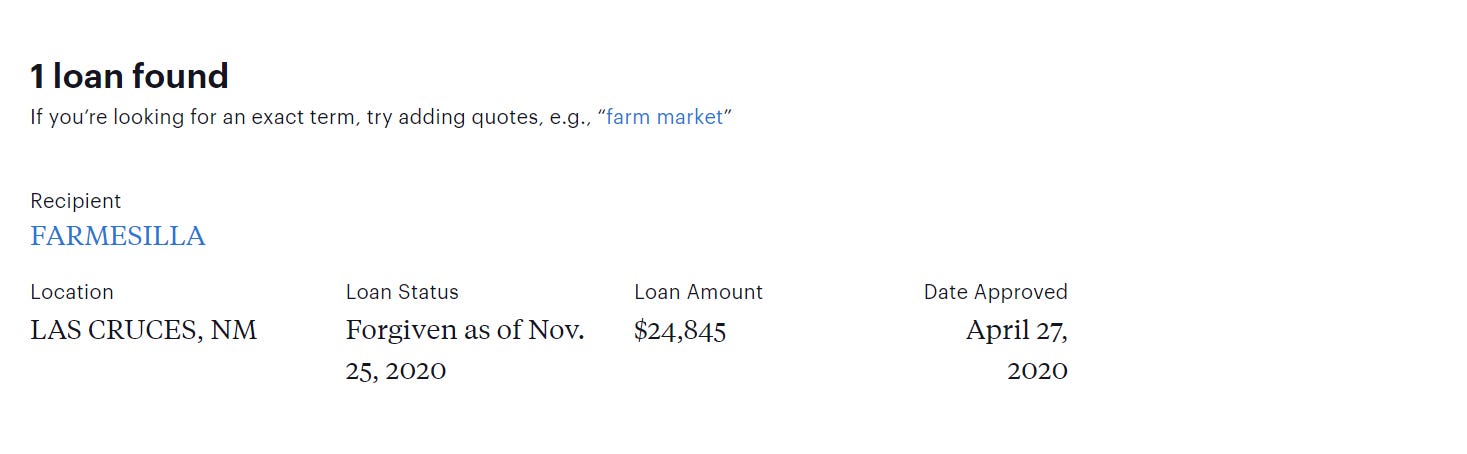

You got a fully forgiven PPP loan. That’s fine. I got people millions in PPP loans across this country by teaching them how to save their business!

But if blue corn flour costs 30% more now than it did in 2020, and the way you go about charging me for it is to blame a bank and my credit card to the tune of 1-2% more than usual because you decided to use a trope of banks sucking (which they do) to justify your inflated costs because of the high-end stuff you have? Then I have a problem with that.

But here’s the thing, I would have still gone to your business regardless because I really like the ideas that you have, despite the money grab.

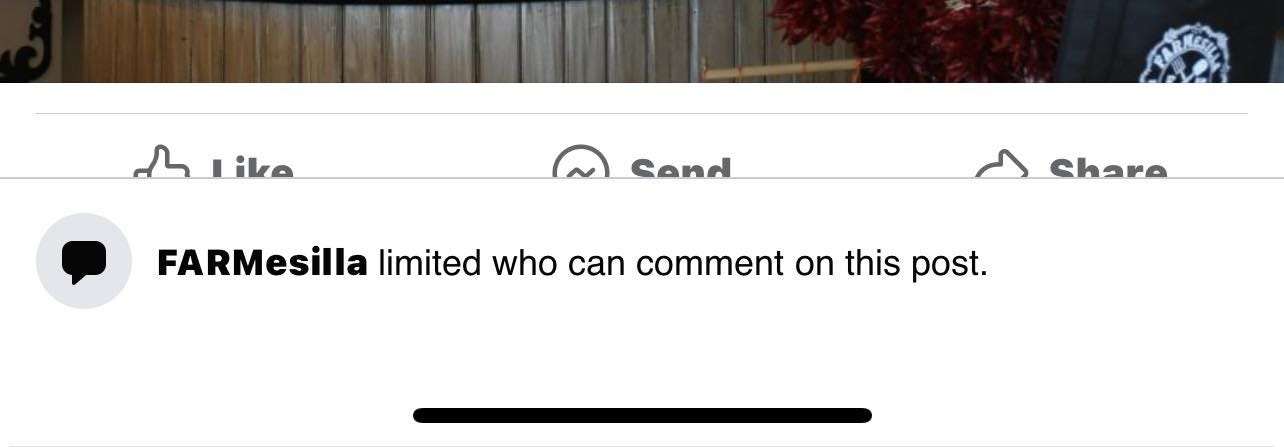

…But then in your post asking people to understand you, especially after you poured your heart out trying to explain why you needed to charge this fee, you do this..

Aw, shucks. You limited who can complain about something. It is the Facebook equivalent of the manager saying “talk to the hand” if I had a complaint about something in person. Aw, gee. It’s a shame. I wanted to support you even though you were wrong about the fee.

Folks, as a former manager, and someone who has a “small business” discussing good customer service and how to make customer experience special, this is the worst kind of foul. Not the 3.5%. Who cares? Your limiting comments told me to shut up, and that’s something that is unethical and unacceptable to me. So, I am officially done with FARMesilla, and I hope you are too, even if they got rid of the fee, because they basically tried to silence customer concerns.

In closing, I understand margins are tight, but this is when good business skills need to shine. Throwing money at a problem doesn’t fix a problem. You need to see if your model for a business is working if 3.5% is going to f^%$ing destroy you like they are claiming. Eliminate things that aren’t selling. Look at other elements of what you spend to open your restaurant. Think like Robert Irvine!

There’s a prominent burger joint in El Paso that I loved. They started charging a CC surcharge as well. 75%, which on a $7 burger is more than 10%. But when I went to a bank meeting and told my boss “I got stuck in traffic” I went to this burger place to get my fix. MMMM..

I knew about the fee, but I was rarely in EP by myself, so I wanted to treat myself, fee and all. I got the receipt from the girl and I got my burger order on there. It’s right. the 75 cent charge was actually masked under “add cheese”. While I got cheese on my burger, there was two cheese charges, and the other one was 25 cents. They had the fee hidden and claimed it was my obesity and love for cheese was the reason. Nope. It was your fee and desire to punish the customer.

I never went back, though I smell it right now in my head.

FARMesilla. It won’t be immediate, but you will see this was a fool’s errand and I wish you the best, without my patronage.. Again, not because of the fee at the end of the day, but you told me to shut up about it.

James